Read the full article here.

The Future of Digital Assets Trading – The Banks are Coming

The size of the digital assets market is growing fast. Institutional interest is exploding, and the still limited market size is increasingly viewed as an opportunity for growth rather than a weakness.

With large infrastructure players from traditional finance such as CME, ICE and Fidelity present, we are witnessing a rapid maturation of the digital asset market. There is, however, one group that has been missing: The big banks. This is about to change.

To better serve their customers, a growing list of tier one banks are building out custody solutions and trading capabilities for bitcoin and other digital assets. Some of the banks have been open about their ventures into the digital space, while others have been more secretive. Still, to really participate, there is a need for a proper interbank market in digital assets; a market replicating the structure, liquidity and standards known from traditional FX.

Arcane Research

Arcane Research is a part of Arcane Crypto, bringing quantitatively-driven analysis and research to the cryptocurrency space. After the launch in August 2019, Arcane Research has become a trusted brand, helping clients strengthen their credibility and visibility through research reports and analysis. In addition, we regularly publish reports, weekly market updates and articles to educate and share insights.

Pure Digital

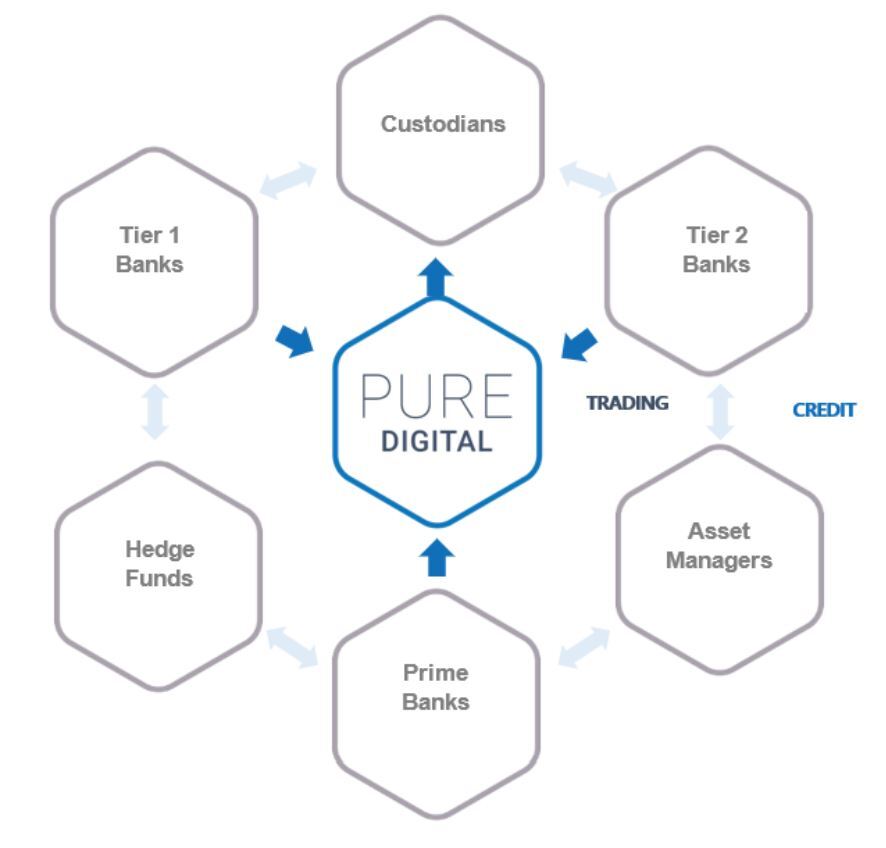

Pure Digital is an interbank marketplace for cryptocurrency price discovery and exchange of wholesale risk. Pure Digital will provide a best-in-class primary institutional market; with a consortium of banks as liquidity providers, custodians, and clearers. Expect meaningful trade size along with price granularity and transparency. The solution also uniquely offers pre-trade bilateral credit and multi/smart custody.

In this report, Arcane Research jumps into the developing story of bank involvement in the crypto world and Pure Digital explains what an interbank market for digital assets will look like.

In this report, Arcane Research jumps into the developing story of bank involvement in the crypto world and Pure Digital explains what an interbank market for digital assets will look like.

Contents

Open Source Finance. 5

Traditional Players are Embracing Digital Assets. 5

Bitcoin – An Appealing Asset 6

The Numbers are Clear – There is Substantial Institutional Interest 6

The Digital Asset Banks are Coming. 9

Traditional Banks are Also Joining. 10

The Evolution of The Market Structure. 10

What an Interbank Market for Digital Assets will Look Like. 13

Utilising the FX Infrastructure Model in Crypto. 13

Market Maturation. 14

Open Source Finance

The digital asset space is characterized by rapid and widespread innovation. The bitcoin whitepaper, an eight-page document shared on an email list for cryptographers twelve years ago, marked the start of a new socio-technological paradigm built around opensource finance often called “the internet of value”.

Where the Internet enabled permissionless innovation and borderless spread of information, bitcoin and its offspring has brought the same possibilities to the realm of digital value.

As a result, bitcoin and the digital assets space represent an evolutionary system, continuously adapting to its surroundings. Bitcoin is neither limited to its founder’s ideas, nor those of some of its early adopters. Instead, bitcoin takes on new capabilities as new people identify and develop new use cases.

A very clear example of this is the recent surge in institutional interest in bitcoin as an uncorrelated (over long timeframes) asset with absolute scarcity, essentially a form of digital gold.

Traditional Players are Embracing Digital Assets

Bitcoin was launched in the midst of the financial crisis of 2008 and was presented as an alternative to the established and centralized financial system. However, as bitcoin has grown ever larger, traditional players have entered the market and are now part of the digital asset space. This is clearly illustrated by the product offerings from leading financial infrastructure providers;

CME Group is the world’s leading and most diverse derivatives marketplace offering the widest range of futures and options products. It launched bitcoin futures in late 2017.

Intercontinental Exchange (ICE), the owner of the New York Stock Exchange, entered the bitcoin space last year when they launched Bakkt. Bakkt began in 2018 with the vision to “bring trust and transparency to digital assets”. Through the Bakkt Warehouse (custody service) and the Bakkt Bitcoin Futures and Options contracts, they now serve institutional clients in an end-to-end regulated market with true price transparency.

Fidelity Investments is one of the largest financial services companies in the world, with $3.3 trillion under management. It’s subsidiary, Fidelity Digital Assets, is now offering enterprise-grade custody and execution services for institutional investors who want exposure to digital assets. Other actors like LMAX, Börse Stuttgart and SIXhave already been in the European market for years with their digital asset offerings.

Previously skeptical banks are now following client demand, building out services for the crypto industry. JP Morgan’s CEO once called bitcoin a fraud, but the company is now accepting bitcoin businesses as customers, taking in both Coinbase and Gemini this year. The company even noted in a recent report that bitcoin could be an alternative to gold:

“Even a modest crowding out of gold as an ‘alternative’ currency over the longer term would imply doubling or tripling of the bitcoin price”

Bitcoin – An Appealing Asset

With better infrastructure comes more attention. It is clear that institutional investors are following this new asset class closely. Over the past two years, Fidelity has interviewed high-net-worth individuals, financial advisors, family offices, crypto hedge and venture funds, traditional hedge funds, endowments and foundations. Fidelity’s recent 2020 survey with almost 800 participants from the US and Europe shows greater interest in and broader acceptance of digital assets as an investable asset class.

- More than 60 percent of the investors feel digital assets have a place in portfolios

- Almost 80 percent of the investors find something appealing about digital assets. The most appealing characteristics are the lack of correlation with other asset classes, exposure to an innovative technology play and high potential upside.

Institutional investors start to see the potential of digital gold in an ever more digitized world where expansionary monetary policy is the new norm. Earlier this year, the well-known investor, Paul Tudor Jones, said that he has allocated 1-2% of his portfolio in bitcoin, which reminds him of gold back in the day:

“We are witnessing the Great Monetary Inflation — an unprecedented expansion of every form of money unlike anything the developed world has ever seen[… ]. The best profit-maximizing strategy is to own the fastest horse[…]. If I am forced to forecast, my bet is it will be Bitcoin […]. Bitcoin reminds me of gold when I first got into the business in 1976.”

In a more recent interview, Tudor Jones compared bitcoin to investing with Steve Jobs and Apple or investing in Google early:

“Bitcoin has this enormous contingence of really, really smart and sophisticated people who believe in it. It’s like investing with Steve Jobs and Apple or investing in Google early.”

Others have been following Tudor Jones, with the likes of Stanley Druckenmiller and Bill Miller stating that they own bitcoin and recommend it. Stone Ridge, Guggenheim and Pendal Group are all moving into bitcoin, with the latter describing that the move was prompted by client demand. In addition, names like Blackrock and Alliance Bernstein are warming up to the idea.

The Numbers are Clear – There is Substantial Institutional Interest

This year is different from what we’ve seen earlier. While institutions entering bitcoin has been a talking point for several years, this is actually reflected in the data in 2020. We now have several different sources showing growing institutional demand for digital assets in general and bitcoin in particular.

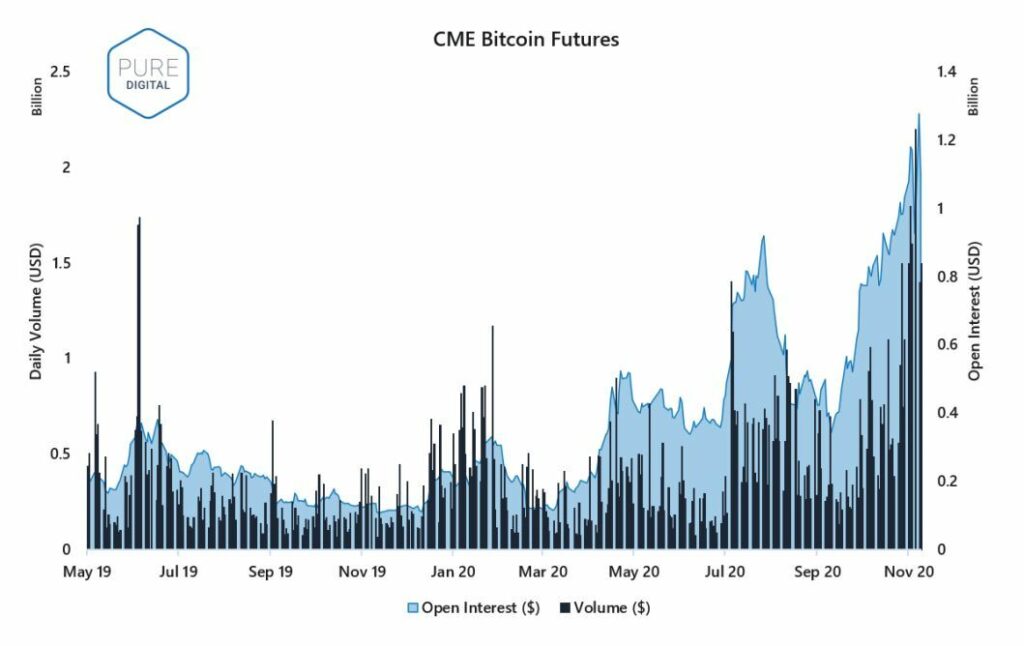

CME is the leading regulated platform for institutional investors who want exposure to bitcoin. This year, the inflow of new money to the platform has been enormous. The Open Interest, measured in USD, tells us how much money is placed in bitcoin futures contracts. From January to May, we saw new all-time highs on several occasions.

Perhaps driven by Tudor Jones entry in May, over $500 million were placed in bitcoin contracts when the summer started. However, after bitcoin jumped to $12,000 in late July, the open interest exploded and topped out just below $1 billion, about 5 times higher than where the year opened.

While decreasing again for a few months, we’re now back above $1 billion in open interest on CME after a massive increase lately. Moreover, the daily trading volume on CME has recently pushed above $1 billion as well, with numerous days closer to $2 billion.

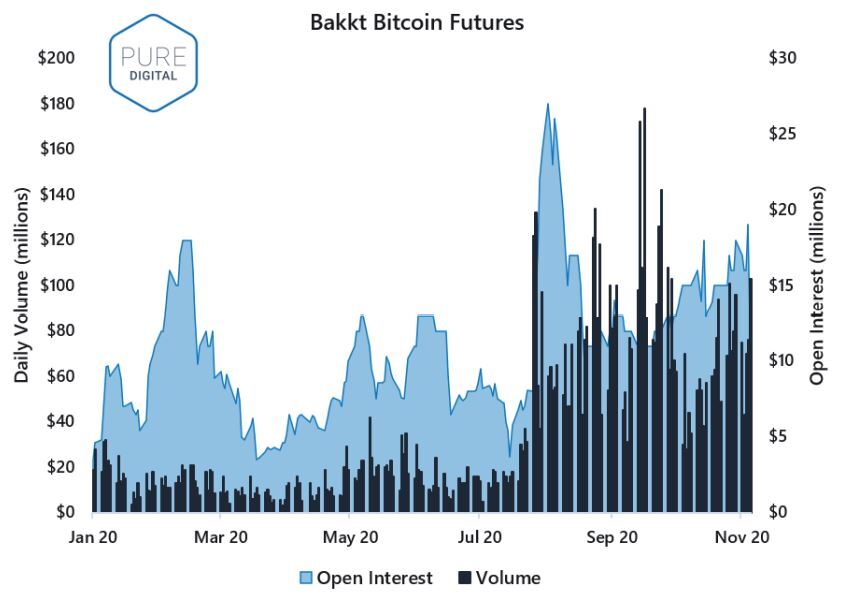

We can see the same kind of growth on Bakkt. While the numbers are still low, the growth this year shows more demand for bitcoin among institutional investors. The average daily volume of the past three months was around $75 million. This is almost 4 times higher than the average from the two first quarters of 2020.

Not only are the leading platforms seeing strong growth, other indicators are showing the increased demand for bitcoin exposure as well.

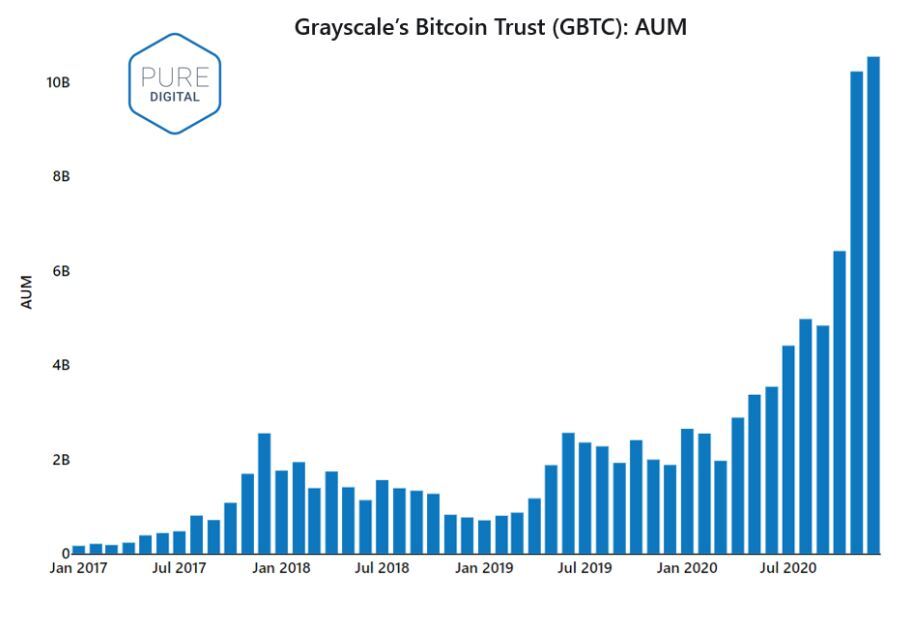

Grayscale Investments has been in the digital assets space since 2013 and has been another company in focus this year. Grayscale allows accredited investors to buy bitcoin and other cryptocurrencies through their investment products.

Their Bitcoin Trust is reaching new highs each month and has just surpassed $10 billion in assets under management. This is backed by bitcoin held by Grayscale, with the company now owning over 540,000 bitcoin – or 2.6% of the current supply.

Not only have we seen more investors wanting exposure to digital assets this year, we have witnessed PayPal offering access to Crypto for payment purposes and also the first publicly traded companies moving cash reserves over to bitcoin.

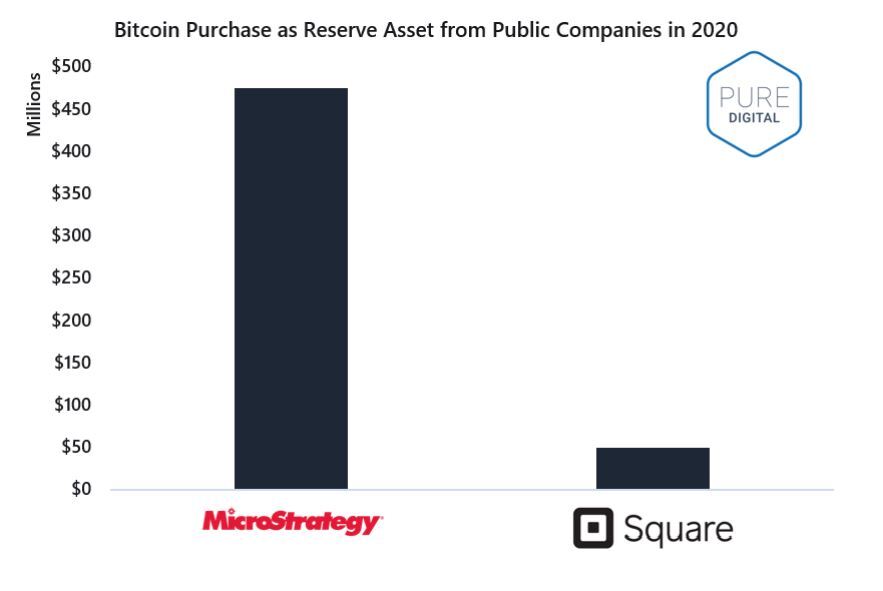

MicroStrategy recently moved 90% of their reserves into bitcoin and is now the owner of more than 40,000 bitcoin, which were bought in three rounds this year, for a total of $475 million. Square Inc, which today operates CashApp, recently bought $50 million worth of bitcoin. These are a couple of the first movers, and we would expect many more to follow suit.

The Digital Asset Banks are Coming

With growing size and institutional interest, the banks are starting to wake up and the first movers are already present and active in the digital assets space. In addition, we are seeing cryptocurrency exchanges moving into banking to leverage their user base and digital asset expertise to launch new products.

Kraken, one of the oldest cryptocurrency exchanges, recently became the first company to be awarded a U.S. banking license in Wyoming. The Wyoming Banking Board voted to approve the application from San Francisco-based crypto exchange Kraken for a Special Purpose Depositary Institution (SPDI) banking charter. This is not a traditional bank charter, so the cryptocurrency exchange cannot issue loans, but the company will get access to the U.S. banking system. This will make it easier to move funds on and off the exchange and opens up the possibility for new products like debit cards, IRA accounts and wealth management services. This will provide a boost for the whole industry and facilitate onboarding for a range of companies and institutions that are only comfortable doing financial transactions with a bank.

In Europe and more specifically in Germany, there is also a growing market and increased interest from banks. BaFin, Germany’s financial regulator, has received more than 40 applications from banks seeking approval to operate a crypto custody business. This news broke in the beginning of 2020, after the new German Anti-Money Laundering Act went into effect, allowing financial institutions to offer their customers cryptocurrencies alongside traditional investment products.

Switzerland is also well-known for its digital asset friendly environment and has seen a lot of financial institutions entering the digital assets space. Basler Kantonalbank, or BKB, a government-owned commercial bank in Switzerland, is planning to launch digital asset services through its banking subsidiary. According to BKB, this is a response to an increase in demand for cryptocurrency services in the country:

“In the BKB Group, we are working to offer our clients a solution for the trading and deposit of selected cryptocurrencies. As an established regional (Basler Kantonalbank) and indeed national (Bank Cler) banking group, we wish to give our clients secure access to these new financial products.”

Julius Baer, a top-five Swiss bank, saw its net profit climb by 34% in the first half of 2020, a period during which it began offering digital asset services to its clients.

Another Swiss company worth mentioning is the digital asset friendly bank Sygnum, which claims to be the first of its kind. The bank has been aggressively expanding its services after obtaining a Swiss banking license in August 2019 and announced that it received regulatory approval to expand its services to a digital asset trading facility a few months ago.

Moving further east, there are also exciting developments. After the Supreme Court in India overturned the central bank’s ban on banking services for digital assets companies in March this year, a lot has happened. India will soon have cryptocurrency financial services offered at more than 20 physical bank branches. The joint venture, called UNICAS, will offer crypto savings accounts and make lending with gold, cryptocurrency and property as collateral available, in addition to cryptocurrency investments.

Traditional Banks are Also Joining

It is not only new and smaller players entering crypto banking. Large, traditional banks have also moved closer to the field of digital assets and especially within custody offerings.

As already mentioned, JP Morgan has taken on cryptocurrency companies as customers this year. The large Japanese investment bank, Nomura, has been in the space for several years already and is part of a newly launched digital assets custodian for institutional investors.

The British banking giant Standard Chartered is building a cryptocurrency custody solution for institutional investors through its Singapore-based venture arm.

One of America’s oldest banks, State Street, teamed up with Gemini Exchange last year to launch a digital assets pilot. The project claims to be a first of its kind and helps building a bridge to the future of money according to Gemini CEO Tyler Winklevoss:

“This joint pilot enables an institutional investor to test custody of digital assets via Gemini Custody and receive reporting for these assets via State Street using two trusted and regulated financial institutions — helping us build a better bridge to the future of money.”

The latest news from traditional banks is related to the largest Southeast Asia bank, DBS, who plan to launch a cryptocurrency a digital assets platform. According to a cached web page, apparently posted in error and then taken down, DBS Digital Exchange will offer access to “an integrated ecosystem of solutions to tap the vast potential of private markets and digital currencies.”

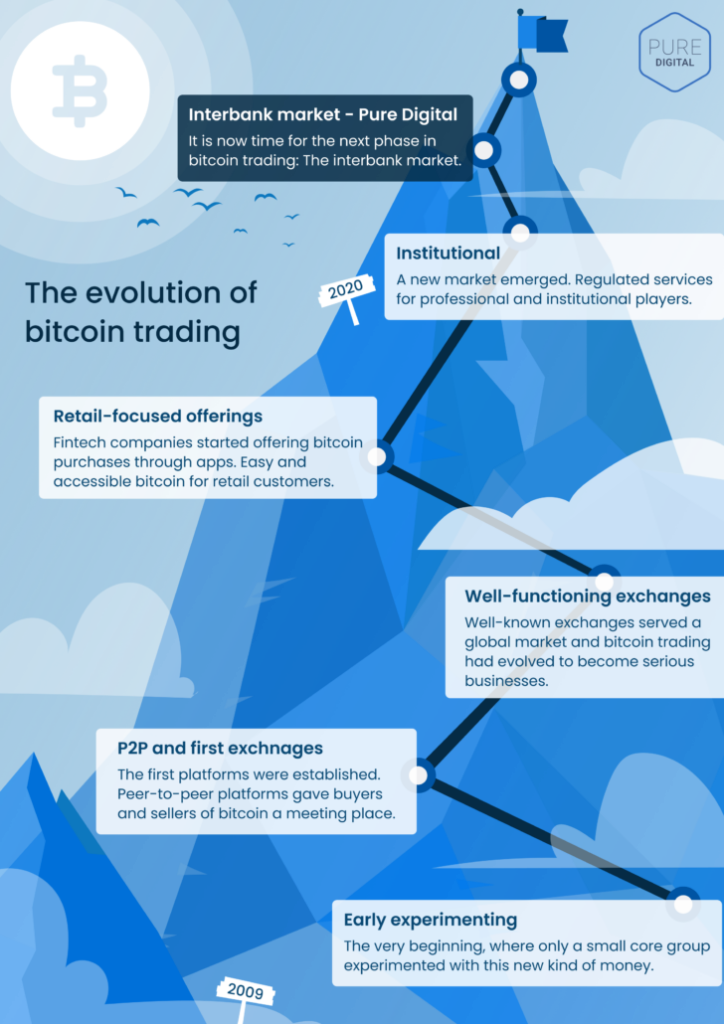

The Evolution of The Market Structure

Without the possibility of exchange, digital assets are worthless. You cannot eat your bitcoin or live in it, so the only way to derive value is in exchange for some other good or service.

As such, the market for trading is as fundamental to the digital asset space as the cryptographic networks, or the blockchains if you like. Much in the same way that the digital assets space has evolved as new types of players have come in, so too has the supporting market infrastructure. There is a strong feedback mechanism between the infrastructure and participation. As more players are joining the digital asset space, more resources are devoted to build out better market infrastructure, and with better infrastructure, more players are joining. In addition, there is a feedback mechanism linked to liquidity and market efficiency. The liquidity improves as more players are joining the market, and more players are joining as the liquidity gets deeper.

Looking at the history of bitcoin, it is clear that the feedback mechanism described above has driven the bitcoin and digital assets market through several distinct phases, with different types of infrastructure serving the needs of different types of players. Serving different needs, the phases are complimentary rather than substitutions.

With banks now on their way into the market, the next phase is likely to be the emergence of a proper interbank market.

Early experimenting

The very beginning, where only a small core group experimented with this new kind of money. At that time, you needed to know someone to trade bitcoin, as there were no public platforms for this.

P2P and first exchanges

The first platforms were established. Peer-to-peer platforms like LocalBitcoins gave buyers and sellers of bitcoin a meeting place. Mt. Gox established itself as the leading exchange and was handling over 70% of all bitcoin transactions worldwide by 2013 and into 2014.

Well-functioning exchanges

Well-known exchanges like Bitfinex, Bitstamp, Kraken and Coinbase served a global market and bitcoin trading had evolved to become serious businesses on well-functioning exchanges.

Retail-focused offerings

Fintech companies like Revolut and CashApp started offering bitcoin purchases through apps. Easily accessible bitcoin for retail customers.

Institutional

A new market emerged. Regulated services for professional and institutional players. Fidelity launched a digital asset offering. CME Group entered the bitcoin futures market and marked the start of a regulated and trusted environment for bitcoin trading. ICE launched Bakkt, a futures market for bitcoin with “physical” delivery, and banks in the US were cleared to custody cryptocurrency.

Interbank market

It is now time for the next phase in bitcoin trading: The interbank market.

What an Interbank Market for Digital Assets will Look Like

Logically, the proven, robust, and well-functioning market infrastructure of the global interbank FX market should be adopted into the digital asset trading ecosystem. With it come significant elements to enable digital trading markets to grow, therefore aiding general adoption and operation of crypto on a more widespread basis.

Utilising the FX Infrastructure Model in Crypto

A properly functioning wholesale interbank spot market will compliment and support existing derivatives venues such as the CME and Bakkt. The institutional market will finally have much needed price discovery along with reliable, transparent, and accurate market data. Bank-grade AML, KYC and onboarding procedures will allow ease of access and security for large, new participants in the market.

The setup will also enable institutional-grade prime brokerage services, ensuring efficient leverage of credit to existing bank clients who will enjoy seamless, stable, and secure access to this new financial asset class. Large balance sheet participants (banks) can bring a vital new control mechanism over which participants they need to trade with.

Importantly, transposing FX infrastructure allows for bilateral credit extension between counterparties. Banks will be able to hand-select counterparties in which they choose to deal or not to deal with.

Lastly, different from existing crypto exchanges, not only can banks decide with whom they trade with, but funds are moved and held outside of the venue. This raises the quality bar by solving custody concerns via a multi-custodial solution, with banks themselves as custodians. All together offering a more sensible marketplace to deliver top banks and their underlying institutional clients what they have been missing.

Market Maturation

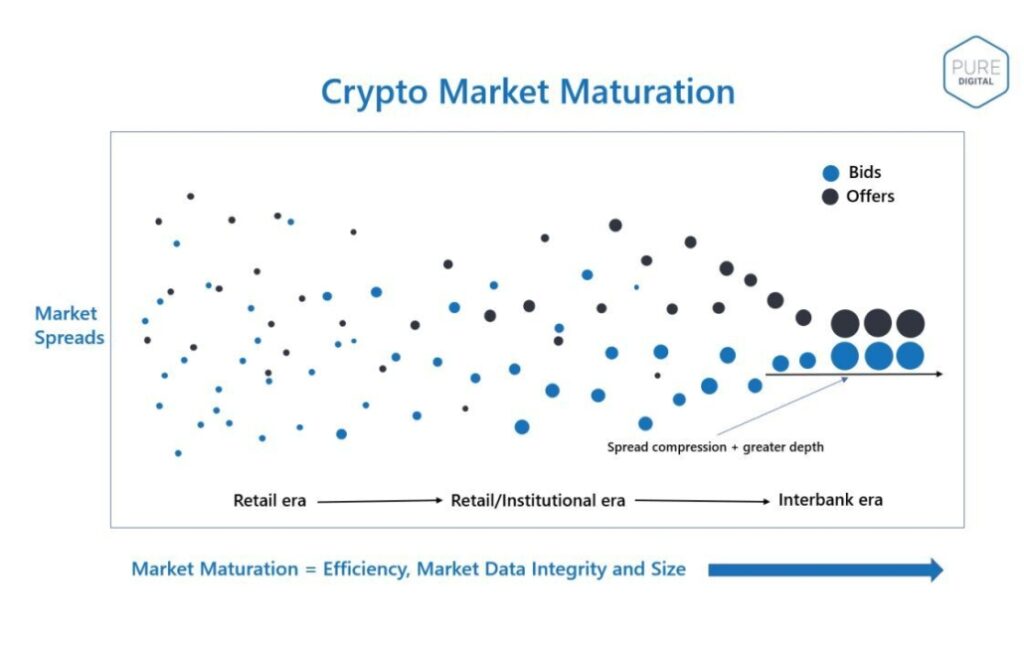

The efficiency of any market is measured by 3 key factors:

- Bid/Offer Spread – the price difference between selling and buying

- Market depth – the quantity that can be bought or sold at the bid or offer

- Integrity of market data – price stability derived from trading activity

As a market matures each of these metrics will improve. This will certainly be the case in the crypto market as it moves into the natural next evolutionary phase, the interbank era. The chart below illustrates how these 3 efficiency factors evolve as banks enter the market.

- Bid/Offer spread compresses

Blue bid and black offer “dots” moving closer

- Market depth increases

Shown by bigger sized Bid/Offer “dots”

- Market data integrity improves

As bid/offer mid-point volatility stabilises

Disclaimer

- The Future of Digital Assets Trading (the “Report”) by Arcane Research and Puremarkets Limited is a report focusing on cryptocurrencies. Information published in the Report aims to spread knowledge and summarise developments in the cryptocurrency market.

- The information contained in this Report, and any information linked through the items contained herein, is for informational purposes only and is not intended to provide sufficient information to form the basis for an investment decision nor the formation of an investment strategy.

- This Report shall not constitute and should not be construed as financial advice, a recommendation for entering into financial transactions/investments, or investment advice, or as a recommendation to engage in investment transactions. You should seek additional information regarding the merits and risks of investing in any stock, commodity, cryptocurrency or digital asset before deciding to purchase or sell any such instruments.

- Cryptocurrencies and digital assets are speculative and highly volatile, can become illiquid at any time, and are for investors with a high risk tolerance. Investors in digital assets could lose the entire value of their investment.

- Information contained within the Report is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made as of the date of publication and are subject to change without notice.

- The information contained in this Report may include or incorporate by reference forward-looking statements, which would include any statements that are not statements of historical fact. No representations or warranties are made as to the accuracy of these forward-looking statements. Any data, charts or analysis herein should not be taken as an indication or guarantee of any future performance.

- Neither Arcane Research, Arcane Crypto AS, nor Puremarkets Limited provide tax, legal, investment, or accounting advice and this report should not be considered as such. This Report is not intended to provide, and should not be relied on for, tax, legal, investment or accounting advice. Tax laws and regulations are complex and subject to change. To understand the risks you are exposed to, we recommend that you perform your own analysis and seek advice from an independent and approved financial advisor, accountant and lawyer before deciding to take action.

- Neither Arcane Research, Arcane Crypto AS, nor Puremarkets Limited will have any liability whatsoever for any expenses, losses (both direct and indirect) or damages arising from, or in connection with, the use of information in this Report.

- The contents of this Report unless otherwise stated are the property of (and all copyright shall belong to) Arcane Research, Arcane Crypto AS and Puremarkets Limited. You are prohibited from duplicating, abbreviating, distributing, replicating or circulating this Report or any part of it (including the text, any graphs, data or pictures contained within it) in any form without the prior written consent of Arcane Research, Arcane Crypto or Puremarkets Limited.

By accessing this Report you confirm you understand and are bound by the terms above.